NOTE: Due to the age of the following post, some of the embedded links may no longer be active. We do apologize. ~ Ed.

When war broke out in 1861, the federal government was without its own money machine, though that would soon change. As expenses from the war mounted, the U.S. government once again issued Treasury Notes to help finance it. The Act of July 17, 1861 authorized Secretary of the Treasury Salmon P. Chase to issue notes at 7.30%, a rate chosen to make interest calculation so easy they would circulate as money — a $50 note accrued interest at a penny a day, for example. Though the seven-thirties, as they were called, didn’t circulate, the same Act provided for the issuance of Demand Notes that did circulate. As their name implies, Demand Notes were redeemable in specie, but that promise was broken by December, 1861 when the government suspended specie payment.

With no money to fund the war, the Union government could either end it or get creative with money. For the Republicans, it was not really a choice. [1]

In January, with Demand Notes eroding in value, Lincoln turned to former political rival Colonel Edmund Dick Taylor, the only man to ever beat him in an election (1832), who suggested the government issue new Treasury notes bearing no interest but printed “on the best banking paper.” Lincoln took his advice, and on February 25, 1862 signed the First Legal Tender Act authorizing the Treasury to issue a fiat paper currency that rose to infamy under the name of “greenbacks.” In appearance, the greenback was almost indistinguishable from the Demand Note. Where the five-dollar Demand Note bore the inscription, “payable to the bearer five dollars on demand,” a greenback of the same denomination had the same message, minus the “on demand” part. This slight omission meant “guns and badges” would now replace gold.

In January, with Demand Notes eroding in value, Lincoln turned to former political rival Colonel Edmund Dick Taylor, the only man to ever beat him in an election (1832), who suggested the government issue new Treasury notes bearing no interest but printed “on the best banking paper.” Lincoln took his advice, and on February 25, 1862 signed the First Legal Tender Act authorizing the Treasury to issue a fiat paper currency that rose to infamy under the name of “greenbacks.” In appearance, the greenback was almost indistinguishable from the Demand Note. Where the five-dollar Demand Note bore the inscription, “payable to the bearer five dollars on demand,” a greenback of the same denomination had the same message, minus the “on demand” part. This slight omission meant “guns and badges” would now replace gold.

{kind=link}

The greenbacks kept the blood flowing on the battlefields, but their proliferation also caused wholesale prices to soar. [2] Also, from the perspective of certain bankers, the greenbacks were fundamentally flawed because they were government fiat money instead of bank fiat money. Their objection, in other words, was not over the ruinous (and unconstitutional) policy of issuing irredeemable paper money, but who would benefit from it–the government or the bankers.

The idea of issuing more debt instead of printing greenbacks was gaining favor in high places. Following Lincoln’s call for an “organization of banking associations” in his State of the Union address of December, 1862, the government established the National Banking System on February 25, 1863.

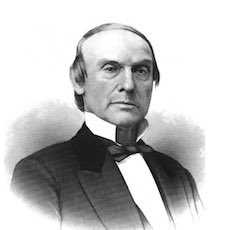

The banker who profited most from the new system was also its chief architect, Jay Cooke. When Lincoln first took office, Cooke had lobbied hard to get Chase appointed as Secretary of the Treasury. After forming the investment banking house of Jay Cooke & Co., Cooke convinced Chase, in the Fall of 1862, to make the House of Cooke the monopoly underwriter of public debt, bestowing on Jay Cooke the title of United States Subscription Agent. Then Cooke and his brother Henry, who was editor of Ohio’s leading Republican newspaper, along with Treasury Secretary Chase and Ohio Senator John Sherman, pedaled the proposed banking system to a reluctant Congress as simply an emergency scheme for funding the war. The Cooke brothers were paying large fees to newspapers for advertising the bonds they were selling, which made it relatively easy to promote their national banking scheme in the editorial pages. [3]

The bank acts of 1863-1865 established the National Banking System and authorized the Comptroller of the Currency to charter national banks. By law, any bank meeting the requirements could be chartered, but the reserve and capital requirements were so high as to rule out small national banks, and many state banks elected not to join the new system. Under this new arrangement, the Independent Treasury, which had funded the Mexican War without inflation, was suspended, with Treasury funds now kept in a tripartite hierarchy of “pets,” which were the nationally chartered banks. State banks could still issue notes, but after March 1865, Congress imposed a 10 percent tax on all state notes, in effect giving the nationals a legal monopoly to issue bank notes. While the new system was sold to the public as a war emergency, its political purpose, according to Senator Sherman, was to “nationalize American politics.” [4]

The truth of Sherman’s statement is reflected in the relationship between the national banks and the national government. National banks could expand their note issue only to the extent they monetized the public debt. The more debt they purchased, the more they could inflate, and when carried out by the larger Wall Street banks, it allowed other nationals to create additional inflation through the mechanism of reserve pyramiding. [5] Thus, the banks could engage in what they perceived as low-risk inflation, while giving the government an assured market for its debt.

The printing of greenbacks, which was discontinued in mid-1863, accounted for only $430 million of the $2.61 billion accumulated war deficit. [6] Along with gold and silver, greenbacks were considered lawful money and could be part of a bank’s reserves. National bank notes themselves possessed some of the privileges of legal tender: the government required all the national banks to accept each other’s notes at par, and it agreed to accept each national bank’s notes at par in taxes. And to minimize the threat of redemption, the government maintained its pre-Civil War policy of keeping branch banking illegal, which forced note holders to go to a bank’s home office for redemption, while making it difficult for any one bank to clear the notes of the others. In addition, the government imposed a $3 million per month maximum limit on net note contraction, which thereby placed a limit on the amount of notes they were required to redeem for specie. [7]

The House of Cooke feasted on this new system. Not only did Cooke “sell the national banks their required bonds, he also set up new national banks which would have to buy his government securities. His agents formed national banks in the smaller towns of the south and west. Furthermore, he set up two large national banks, the First National Bank of Philadelphia and the First National Bank of Washington, D.C.” [8]

Cooke’s bond sales ranged between $1 to $2 million a day, and by war’s end, the House of Cooke had underwritten nearly $2 billion in bonds. [9] Though he lost his monopoly for a year in 1864, he remained in that privileged position until the Panic of 1873 closed his banking operation. The financier of the Civil War, who had made millions with his pyramided system of fractional-reserve lending, filed for bankruptcy on September 18, 1873.

Asking who paid for the war is misleading; in a very real sense we’re still paying for it and will be until we return to sound money – money, in von Mises’ words, that obstructs “the government’s propensity to meddle with the currency system.” [10]

But for the powers-that-be, the idea of sound money bordered on academic. What was clearly not academic was the fatal flaw in the National Banking System. Granted, the system of national paper money and pyramided reserve banking had financed a major war and made certain men very rich. But any scheme that left the country’s biggest financier bankrupt was destined to be short-lived. Ironically, Progressivism, the turn-of-the-century movement that sought to bring down the fat cats, provided the political means to raise them to new heights. [11]

~ References ~

1. G. Edward Griffin, The Creature from Jekyll Island: A Second Look at the Federal Reserve, Fourth Edition, American Media, Westlake Village, CA, 2002, p. 383

2. Murray N. Rothbard, The Mystery of Banking, Mises Institute, Auburn, AL, 2008, pp. 219-220

3. Ibid., pp. 223-224

4. Murray N. Rothbard, A History of Money and Banking in the United States: The Colonial Era to World War II (pdf), Mises Institute, Auburn, AL, 2002, p. 136

5. Mystery, p. 225; History, pp. 138-141

6. Mystery, p. 220

7. Murray N. Rothbard, The Case Against the Fed, Mises Institute, Auburn, AL, 1994, pp. 77-78

8. History, p. 146

9. Mystery, p. 221

10. Ludwig von Mises, The Theory of Money and Credit, The Foundation for Economic Education, Inc., Irvington-on-Hudson, New York, 1971, p. 414

11. Gabriel Kolko, The Triumph of Conservatism: A Reinterpretation of American History, 1900-1916, The Free Press, New York, NY, 1977.

Written by George F. Smith and published by 24h GOLD ~ May 20, 2011