Few areas of historical research have provoked such intensive study as the origins and causes of America’s Great Depression. From 1929 to 1933, America suffered the worst economic decline in its history. Real national income fell by 36 percent; unemployment increased from 3 percent to over 25 percent; more than 40 percent of all banks were permanently closed; and international investment and trade declined dramatically.

Few areas of historical research have provoked such intensive study as the origins and causes of America’s Great Depression. From 1929 to 1933, America suffered the worst economic decline in its history. Real national income fell by 36 percent; unemployment increased from 3 percent to over 25 percent; more than 40 percent of all banks were permanently closed; and international investment and trade declined dramatically.

The dimensions of the economic catastrophe in America and the rest of the world from 1929 to 1933 cannot be captured fully by quantitative data alone. Tens of millions of humans suffered intense misery and despair. Because of this trauma, the Great Depression has dominated much of the macroeconomic debate since the mid-20th century.

Sen. Reed Smoot and Rep. Willis C. Hawley, April 11, 1929

In 1930, a large majority of economists believed the Smoot-Hawley Tariff Act would exacerbate the U.S. recession into a worldwide depression. On May 5 of that year, 1,028 members of the American Economic Association released a signed statement that vigorously opposed the act. The protest included five basic points. First, the tariff would raise the cost of living by “compelling the consumer to subsidize waste and inefficiency in [domestic] industry.” Second, the farm sector would not be helped since “cotton, pork, lard, and wheat are export crops and sold in the world market” and the price of farm equipment would rise. Third, “our export trade in general would suffer. Countries cannot buy from us unless they are permitted to sell to us.” Fourth, the tariff would “inevitably provoke other countries to pay us back in kind against our goods.” Finally, Americans with investments abroad would suffer since the tariff would make it “more difficult for their foreign debtors to pay them interest due them.” Likewise most of the empirical discussions of the downturn in world economic activity taking place in 1929–1933 put Smoot-Hawley at or near center stage.

Economists today, however, hold a different view of the effects of Smoot-Hawley. While economic historians generally believe the tariff was misguided and may have aggravated the economic crisis, the consensus appears to relegate it to a minor status relative to other forces. We believe many modern economists are wrong because flawed modeling leads to two systematic understatements of the tariff’s negative effects. The first reason for this is that reliance on macro aggregates can sometimes mask serious underlying problems by dissipating their apparent impact over a broad area. For example, U.S. national income declined 36 percent in real terms from 1929 to 1933, and the view held by prominent economists, ranging from University of Chicago Nobel laureate Robert Lucas and Yale economist Robert Shiller to MIT economists Rudiger Dornbush and Stanley Fischer, is that since the foreign-trade sector was only about 7 percent of gross national product (GNP), the tariff (though misguided) could not explain much of this decline.

Viewed at the level of “macro magnitudes,” critical micro connections suffer from a “dissipation effect” and always look small. But size does not equal significance. While it is true that foreign trade represented only a small percentage of the overall domestic and international economy, it does not follow that the tariff was insignificant in its effects. The Panama Canal contains but a small fraction of the world’s ocean water, but if it were closed the effects would be quite devastating to world trade. A focus on aggregates risks missing the trees for the forest, and not all trees are created equal.

Here’s a second way Smoot-Hawley is underestimated: If regulations or tariffs are studied in partitioned models, their interrelationships are missed and their true impacts are trivialized. For example, recent attempts have been made to quantify price distortions caused by the tariff. Mario Crucini and James Kahn have tried to correct systematic underestimates of the harm of Smoot-Hawley found in a variety of macro studies that ignored the effect of tariff retaliation on the rate of capital accumulation. Using a general-equilibrium model, they calculate that the microeconomic distortion effects reduced U.S. GNP by only 2 percent in the early 1930s. Likewise, economist Douglas Irwin computed the general-equilibrium inefficiencies caused by the tariff at nearly 2 percent of GNP.

So when even ostensibly free-market, free-trade economists such as Lucas, Irwin, and others downplay the negative effects of the Smoot-Hawley Tariff, what’s the verdict? Were the loud protests of over a thousand professors of economics just unsophisticated exaggerations? Were these pre-Keynesian classical theorists misguided because they lacked the tools of modern macroeconomics and econometrics? Or did their vision remain unclouded for the same reason? Were they Chicken Littles or Cassandras?

Ignored Effects

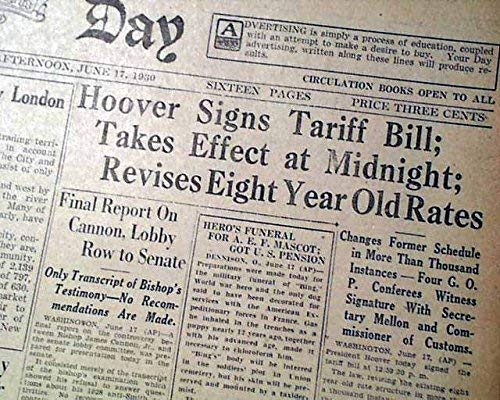

Modern measurements of Smoot-Hawley often ignore a wide range of important negative effects. For instance, the secondary financial markets, such as the New York Stock Exchange, crashed twice during the last eight months of Smoot-Hawley’s legislative history. Jude Wanniski and Scott Sumner have linked concern over the impending tariff to the October 1929 crash and the June 1930 crash. The Dow Jones Industrial Average fell 23 percent in the first two weeks of June 1930 leading up to President Herbert Hoover’s signing the bill into law. On June 16 Hoover claimed, “I shall approve the tariff bill,” and stocks lost $1 billion in value that day – a huge sum at the time.

Furthermore, if losses of GNP were not evenly distributed across the economy but were concentrated (say, in export-oriented states), the tariff most likely distorted monetary conditions significantly. Two percent of GNP does not sound like a big change, but if it’s concentrated in one-fifth to one-third of the states, it’s very large indeed. The tariff dramatically lowered U.S. exports, from $7 billion in 1929 to $2.4 billion in 1932, and a large portion of U.S. exports were agricultural; therefore, it cannot be assumed that the microeconomic inefficiencies were evenly distributed. Many individual states suffered severe drops in farm incomes due to collapsing export markets arising from foreign retaliation, and it’s no coincidence that rural farm banks in the Midwest and southern states began failing by the thousands.

Agriculture was not the only export sector destroyed by the tariff. The worldwide retaliation against U.S. minerals greatly depressed income in mining states and can be partially blamed for the collapse of the Wingfield chain of banks (about one-third of the banks in Nevada, with 65 percent of all deposits and 75 percent of commercial loans). U.S. iron and steel exports decreased 85.5 percent by 1932 due to retaliation by Canada. The cumulative decrease in those exports below their pre-tariff levels totaled $369 million. Is it any wonder that Pittsburgh saw 11 of its largest banks, with $67 million in deposits, close in September 1931? How about U.S.-made automobiles? European retaliation raised tariffs so high that U.S. exports declined from $541 million per year to $97 million by 1933, an 82 percent drop! Thus there was a cumulative export decline of $1.57 billion from the pre-tariff volume to 1933. Is it any wonder that the Detroit banking system (tied to the auto industry) was in complete collapse by early 1933?

Let’s not forget World War I, which made America the world’s creditor. The center of the financial world moved from London to New York, and billions of dollars were owed to large U.S. banks. The Smoot-Hawley Tariff threw inter-allied war-debt repayment relations into limbo by shutting down world trade. An international moratorium on debtor repayments to the United States froze billions in foreign assets, thus weakening the financial solvency of the American banks. Specifically, over $2 billion worth of German loans were obstructed by Germany’s inability to acquire dollars through trade to repay its debts. This same scenario played out in many other countries as well. The tariff wars created widespread financial crises across America, Europe, and a host of nations in South America. In September 1931 England abandoned sound money; America would follow suit in 1933. The functional operation of the post-World War I gold exchange standard was sabotaged by worldwide protectionism in reaction to Smoot-Hawley.

Historians of the Great Depression have overlooked important connections between trade conditions and monetary collapse. The tariff and retaliations against it destroyed the world trade system and demolished the integrated world financial structure operating under the gold-exchange standard as well. America’s monetary and capital structure from 1921 to 1929 was primarily shaped by six factors: first, a centrally planned monetary system; second, a decade of disguised inflation; third, branch-banking restrictions; fourth, state deposit insurance programs; fifth, agricultural subsidies; and finally, a plethora of taxes and regulations.

Smoot-Hawley placed enormous pressure on the central banking system and capital structure. In addition it caused the dramatic loss of export markets and declining farm income (due to foreign retaliation), rendering much agricultural capital useless. This was responsible for widespread agricultural bank failures, which then led to contagion effects. Due to the uncertainty of trade conditions, each of the ten largest world economies had their secondary financial markets crash. It created international financial chaos leading to foreign debt repayment suspensions. As a result of thousands of bank failures, the U.S. money supply dropped 29 percent from 1929 to 1933. (The weighted average of the world money supply of the eight largest economies annually declined by double digits from 1931 to 1932). All of this, and much more – and yet only 2 percent of GNP? We think not.

Macroeconomic Thought and Smoot-Hawley

Modern macroeconomics falls into three broad schools of thought: Keynesian, monetarist (including New Classical), and Austrian. While great differences exist among the different theories of the business cycle, all seem to agree that the tariff had little causal relevance to the severity of the Great Depression. For example, Keynesian Peter Temin never cites the tariff once in his Did Monetary Forces Cause the Great Depression? Likewise Milton Friedman and Anna Schwartz delegate a mere footnote to Smoot-Hawley in their massive treatise, A Monetary History of the United States, 1867–1960. To his credit Austrian economist Murray Rothbard at least devotes one and a half pages to the tariff in America’s Great Depression.

As noted Smoot-Hawley can be directly linked to the U.S. agricultural crisis of the early 1930s and the initial banking crises in a variety of Midwestern agricultural states. Therefore trade policy may have indirectly, but severely, worsened monetary conditions. If the great monetary contraction was an important factor in the severity of the Great Depression, then the Smoot-Hawley tariff must be held responsible in large part. Estimates that downplay the significance of the tariff on aggregate economic activity are dangerous because the correct lessons will not be learned. The relationship between monetary policy and trade policy is not a one-way street. Policymakers speak of affecting the terms of trade by manipulating the money, but they do not realize that their money has become vulnerable to the terms of trade. Modern macro and micro modeling biases preclude economists from seeing this full impact.

The Day, New London, Connecticut, June 18, 1930

Smoot-Hawley and Bank Crises

In 1976 monetarist Allan Meltzer noted, “Given the size of the decline in food exports and in agricultural prices, it is not surprising that many of the U.S. banks that failed in 1930 and in 1931 were in agricultural regions.” Meltzer’s observation indicates that misguided trade policy may have triggered the bank failures and resulting monetary collapse in a significant way. We believe Meltzer’s insight gives us a better understanding of the Great Depression.

The most widely accepted theory for the beginning of the Great Depression is the monetarist narrative, which has the collapsing banking system as the prime causal factor. The empirical evidence suggests that a disguised monetary inflation throughout the 1920s was followed abruptly by an open and severe deflation following 1929. The appreciable financial disintegration and deflation caused by over 10,000 bank failures and an implosion of the inverted credit pyramid certainly had very real negative economic effects.

The thesis that a negative trade shock can impact monetary policy fits these empirical puzzle pieces together. The tariff not only closed off the U.S. export market to farmers, it also left a vast volume of heterogeneous and specific capital goods used in agricultural production idle and suddenly worthless. Empty silos and buildings, rusting tools and machinery, and unused acreage – all in particular geographical regions – led to severe liquidations and farm foreclosures in the states experiencing the first banking crisis, with the vast bulk of failures involving small state-chartered rural banks. Economic historian Eugene White, who examined individual bank balance-sheet data, identifies the agricultural distress in the Midwestern states as a central reason for the pattern of failures. The Smoot-Hawley tariff was a direct factor in both the pattern of failures and their geographic location.

Microeconomic Connections

Here is where the Austrian business cycle model can aid our understanding of the crisis. The monetary theory of capital malinvestment arises from relative price distortions and heterogeneous capital. Both points are by and large absent from most macro modeling of business cycles. These microeconomic connections are, however, fundamental. Disguised inflation in the 1920s probably created a constellation of malinvestments in need of liquidation, meaning that by 1929 a business recession was likely inevitable. However, an extraordinary tariff war brought world trade to a screeching halt. The tariff created additional malinvestment in a capital structure already in need of market readjustments. Both prior monetary inflation and restrictive trade policy led to and exacerbated the economic downturn. They are not mutually exclusive alternatives.

Misguided public policies, such as state-run deposit insurance and branch-banking restrictions, created a banking system vulnerable to pervasive failures caused by adverse trade shocks. The moral-hazard problems associated with inaccurate risk-pricing—and the fragility of the system due to restrictions on geographical risk diversification – would prove fatal. At the same time that intervention was leading rural banks to commit capital to riskier loan portfolios, intervention was exposing them to additional risk. When unexpected changes in regional economic conditions arise from arbitrary interventions in the free-trade system, undiversified banks will fail in large numbers. Smoot-Hawley, one of the most massive tariffs in American history, destroyed an enormous portion of the vulnerable capital structure. The resultant contagion, bank runs, and failures that followed show that trade policy can affect monetary conditions.

Central Bank Illusion

Whether the Federal Reserve could have stopped the contagion and subsequent bank failures misses the main economic point. Central-banking advocates sell an illusion of monetary stability, when in reality the system is wide open to adverse shocks and therefore is highly unstable over the long run. A central bank can easily overexpand or overcontract the stock of money and credit. This is best illustrated by the contrast of the Federal Reserve System to its freer Canadian counterpart. Canada did not have antibranching regulations, socialized deposit insurance, or a central bank. This is significant because over 30 percent of Canada’s GNP originated in foreign trade. Smoot-Hawley escalated tariff barriers between Canada and the United States, yet Canada did not experience any bank failures or bank runs, and its money supply declined by only 13 percent (versus 29 percent in America). There is every reason to believe that a free-banking system most likely would have prevented the disguised inflation of the 1920s and averted the geographical vulnerabilities along with the open secondary deflation characteristic of the 1930s. After World War I many countries tragically established central banks under the illusion that monopoly and central planning in money would lead to economic stability. History has rendered its verdict on central planning: Whether it be shoes, screws, or money, it always fails.

All of which brings us to today. While “welfare-warfare” states throughout the world are running huge fiscal deficits, their central banks are recklessly monetizing massive quantities of debt (inflation). Extraordinary volatility now characterizes financial markets amidst a worsening sovereign debt crisis. Major financial institutions throughout the world hold mountainous portfolios of worthless assets that government policy has steered them into holding. Defaults threaten to destroy the world monetary systems in spite of all the short-run political machinations of prime ministers and central-bank leaders. And in these dangerous waters, what do we hear from the politicians, many already with their hands red? Trade protectionism!

When political agents denounce China on trade and demand an appreciation of its currency, it is the functional equivalent of placing a tariff on each and every Chinese export. This type of protectionist saber-rattling risks igniting not only a destructive international trade war but also, with the economy in the aftermath of a colossal bubble and the world’s banker growing restless with its hoard of depreciating IOUs, vastly more damage than the world is prepared to handle. Have we learned nothing from the past?

Written by Theodore Phalan, Deema Yazigi and Thomas Rustici for the Foundation for Economic Education ~ February 29, 2012